SUMMARY

This blog is written by HPQ CEO Bernard Tourillon. He outlines evidence of coordinated short selling and order book manipulation, arguing that such practices distort fair pricing and penalize innovation. His goal is to expose how these tactics undermine small-cap companies like HPQ and to push for a market that rewards fundamentals, not manipulation.

DEEP DIVE

Spoofing and layering are market manipulation techniques where traders place and quickly cancel orders to create a false impression of market activity and potentially profit from the price movements they induce.

There is a point in every investigation when instinct gives way to evidence. For us, that moment has arrived.

For weeks, I’ve raised concerns about suspicious trading in HPQ shares.

We’ve filed multiple formal complaints with the Canadian Investment Regulatory Organization (CIRO), highlighting spoofing and layering patterns that we observed in our order book. At first, it was about observation and suspicion. Now, we have data to match the behavior.

The Short Sellers Have Made Themselves Visible

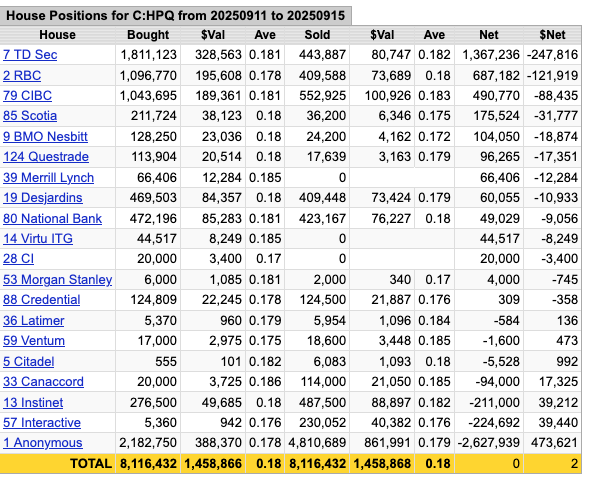

According to official CIRO data, between September 1 and September 15 more than 14.5 million HPQ shares changed hands, most of them trading around $0.16. Included in these trades were 1,262,500 shares declared as short sales to CIRO, meaning that during that two-week period, 9% of all shares traded were reported as short sales, executed at an average trading price of $0.18.

But that is not the real story. Since the short sales were executed at a higher average price than the overall trading that occurred during the covered period, it is clear they took place over a very limited window — in fact, between September 11 and September 15, the same period I had previously highlighted to regulators for suspected illegal spoofing activity.

Unfortunately, the 8.1 million HPQ shares traded at an average price of $0.18 during that period — most likely driven by the positive news issued on September 11, 2025 — were met with a resistance wall of 1,266,432 shares being shorted. This means that the percentage of short sales in our volume was not the 9% indicated in the official report, but closer to 15.6%. Short-sale levels above 10% are generally considered a warning sign of abnormal short-selling pressure, and in many cases, they are viewed as indicative of a coordinated short attack. This provides significant additional confirmation that HPQ shares are being artificially held back.

This activity was not random. It clustered around known desks and tactics.

For example, Interactive Brokers (Broker 57) sold over 392,000 shares while buying just over 5,000; Canaccord (Broker 33) sold 114,000 and bought only 2,000. But the most striking case was Broker 1 — the anonymous “house” account used to mask trades — which bought 2.1 million shares while selling 4.8 million. When combined with the timing and structure of these orders, which display classic layering behavior, the evidence strongly indicates that a group of traders is deliberately capping HPQ’s share price.

Screenshot of Trading Workstation

We’ve seen this before, and we’re seeing it again.

Even more troubling is that this shorting wave occurred right as HPQ was releasing positive news. We were reporting progress on our battery materials, announcing project milestones, and preparing for the next phases of monetization. Instead of the market responding accordingly, we were met with artificial sell pressure, visible order book manipulation, and broker activity that appears coordinated and strategic.

The strategy is clear: build large, non-executable sell orders during pre-market, drive sentiment lower, and layer additional ask pressure during key trading windows. Once the price begins to crack, open short positions into the weakness and cover as retail exits.

This is not theory.

This is what the numbers now confirm.

What This Means for HPQ—and for Every Small-Cap Innovator

Short selling, when used properly, is a tool for liquidity. But in our case, and in the case of many Canadian small-cap issuers, it has become a tool for control. It is being used not to manage risk, but to manufacture it. It damages investor trust, weakens valuations, and threatens the viability of companies working to bring real innovations to market.

HPQ is an R&D-first company. Our work in silicon-based anodes, fumed silica, and hydrogen production is serious and ongoing.

We are delivering technical results, filing patents, and preparing for scale-up. These are not promotional efforts, they are concrete business developments. And yet, our share price has faced pressure that cannot be explained by fundamentals or natural supply and demand.

Some may ask, “why keep pointing this out publicly?”

My answer is simple: because silence has consequences.

If we allow this type of behavior to continue unchecked, we normalize it. And if we normalize it, we effectively punish any company trying to do things the right way.

This is not only about HPQ anymore. This is about what kind of market we want. Do we want a capital market where innovation, performance, and transparency are rewarded? Or one where visibility makes you a target, and success is treated as an opportunity to exploit liquidity gaps?

I will keep pushing because I believe in the former. And I believe that investors deserve better.

Over the last 35 years, Mr. Tourillon has held senior-level executive positions with extensive finance, accounting, marketing, administration, and business development experiences in diverse industries including banking, manufacturing, exploration, mining, and technologies companies. Since joining HPQ Silicon in 2006, he has participated in fundraising activities and financial transactions worth over $49 million.